Why do I have to pay more for Medicare? Can I stay on Obamacare? Is Medicare mandatory?

Turning 65 can be confusing when it comes to your health insurance. Many people are shocked when their costs change, their subsidies disappear, or they hear that Medicare becomes “mandatory.”

Here’s a clear explanation of what really happens and what options you have so you don’t overpay or risk penalties.

1. What changes when you turn 65?

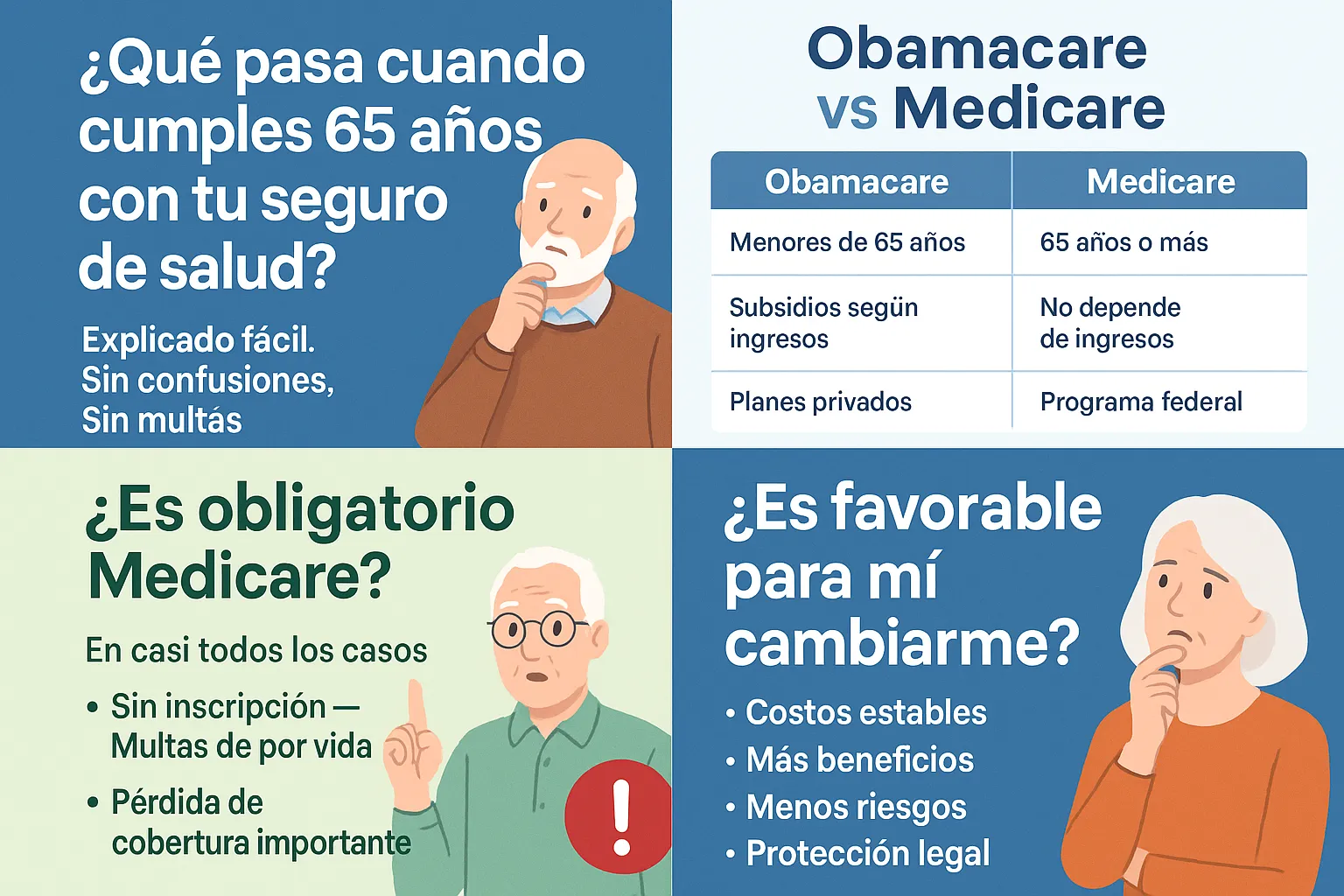

When you reach age 65, the federal government considers you eligible for Medicare, which is a completely different program from Obamacare (Marketplace).

This triggers several changes:

- Your Marketplace subsidy ends.

- Your monthly premium can increase.

- You become eligible (and often required) to move into Medicare.

2. Obamacare vs Medicare — What’s the difference?

Obamacare (Marketplace / ACA):

- For people under 65

- Subsidies based on income

- Private insurance plans

Medicare:

- For people 65+ or disabled

- Federal program

- Costs not based on income (although higher incomes may pay more)

- Divided into Parts:

| Part | Covers |

|---|---|

| A | Hospital care (usually free if you worked 40 quarters) |

| B | Doctors, specialists (monthly premium) |

| D | Prescriptions |

| C (Advantage) | Private plans that combine A+B+D |

3. Why do I have to pay more when I turn 65?

Because when you become eligible for Medicare:

➡️ You no longer qualify for Marketplace subsidies.

➡️ If you stay on Obamacare, you pay the full price of the plan.

This creates the impression that “Medicare is expensive,” when in reality your subsidy disappeared.

4. Is Medicare mandatory?

In most cases: YES.

If you are eligible for Medicare, federal law says:

- You cannot continue receiving Obamacare subsidies

- You may face lifetime penalties if you delay Medicare Part B

- You may lose enrollment windows

5. Can I stay on Obamacare after age 65?

You can stay ONLY if:

✔ You are NOT eligible for Medicare

(For example, you don’t have enough work credits.)

✔ You enroll ONLY in Medicare Part A and NOT Part B

BUT:

- You will NOT receive any subsidies

- You may pay a penalty later

- You won’t have full medical coverage

- Highly not recommended

6. What if I take only Medicare Part A? Can I still get Marketplace insurance?

Technically YES, but:

- You will pay the full premium (no subsidies)

- You may get a lifetime penalty for delaying Part B

- It’s not considered full coverage

This option is usually NOT favorable.

7. So what’s the best option for me?

For most people:

⭐ The recommended path is:

- Enroll in Medicare Parts A & B

- Choose between:

- A Medicare Advantage plan ($0 premium available), or

- A Medicare Supplement (Medigap) + Part D

Benefits include:

✔ Stable costs

✔ More coverage

✔ Extra benefits

✔ No penalties

✔ Federal protection

8. Are there ways to avoid paying more?

YES — in some cases:

✔ If you’re still working and covered by employer insurance

You can delay Part B without penalty.

✔ If you don’t qualify for Medicare

You can stay on Marketplace with subsidies.

✔ If your income is low

You may qualify for programs that pay Part B, Part D, or copays.

9. Need help understanding your case?

At 2JVS Insurance, we help you:

✔ See if you qualify for Medicare

✔ Avoid penalties

✔ Compare options

✔ Check doctors and medications

✔ Find programs that reduce your costs

📞 305-249-1518

💬 Text “65” and get a free consultation.

Leave a Reply